Latest Bank of Canada Business Sentiment

DLC Canadian Mortgage Experts • July 7, 2020

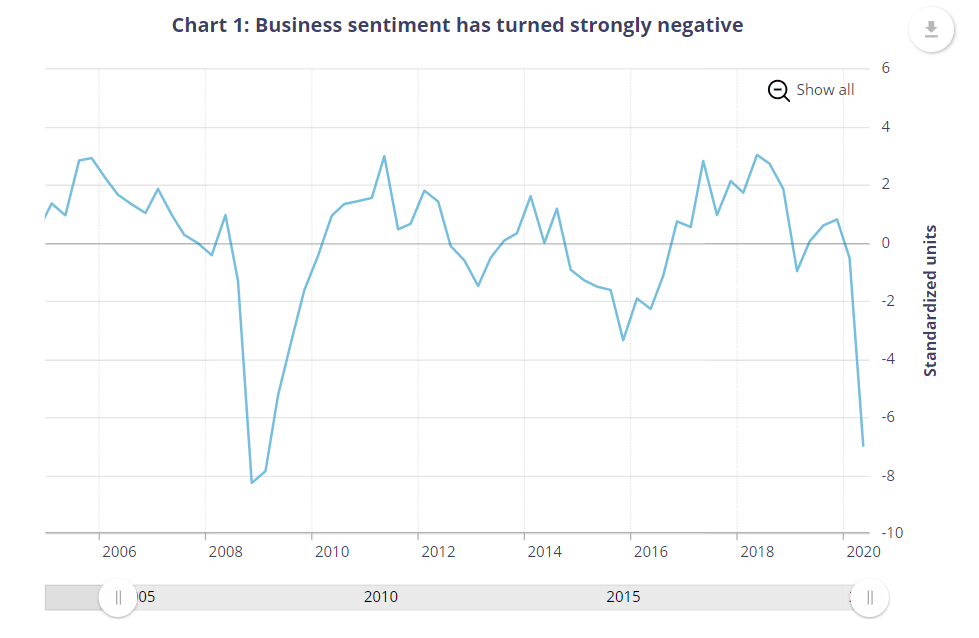

The Bank of Canada released its Summer Business Outlook Survey (BOS)*

this morning, covering an interview period from mid-May to early June. In all provinces and all sectors, the sentiment was hugely negative owing to the impact of the pandemic and falling oil prices.

Since the previous survey, conducted before concerns about COVID-19 has intensified, but as oil prices had already started to fall, business confidence plunged. Surprisingly, however, the business sentiment was not as negative as during the 2007-09 global financial crisis (see Chart 1 below). This was mainly due to the government support offered to cushion the blow of the pandemic. Also, many firms expect a reasonably quick rebound in operations after a temporary decline in sales, unlike the 2007–09 crisis when businesses anticipated persistent weakness in demand.

Highlights of the BOS:

Since the previous survey, conducted before concerns about COVID-19 has intensified, but as oil prices had already started to fall, business confidence plunged. Surprisingly, however, the business sentiment was not as negative as during the 2007-09 global financial crisis (see Chart 1 below). This was mainly due to the government support offered to cushion the blow of the pandemic. Also, many firms expect a reasonably quick rebound in operations after a temporary decline in sales, unlike the 2007–09 crisis when businesses anticipated persistent weakness in demand.

Highlights of the BOS:

- Forward-looking sales indicators have collapsed. Many businesses referred to elevated uncertainty. Still, roughly half of firms anticipate that their sales will recover to pre-pandemic levels within the next year.

- Businesses in most regions and sectors intend to cut their investment spending significantly. Hiring plans are muted, although a quarter of firms plan to refill some positions after recent layoffs.

- Reports of capacity pressures and labour shortages have fallen significantly. This suggests a substantial widening in economic slack.

- Expectations for input and output price growth, as well as for overall inflation, are all down considerably.

- Credit conditions have tightened significantly, but government measures are a helpful offset.

_______________________________

*The Business Outlook Survey summarizes interviews conducted by the Bank’s regional offices with the senior management of about 100 firms selected in accordance with the composition of the gross domestic product of Canada’s business sector. This survey was conducted by phone and video conference from May 12 to June 5, 2020.

*The Business Outlook Survey summarizes interviews conducted by the Bank’s regional offices with the senior management of about 100 firms selected in accordance with the composition of the gross domestic product of Canada’s business sector. This survey was conducted by phone and video conference from May 12 to June 5, 2020.

BoC Consumer Expectations Survey--Q2 2020

This survey was conducted from May 11 to June 1, in the throws of the ongoing pandemic. Of most concern to consumers was the prospect of losing their jobs. Many believed finding another job would be difficult. As well, consumer expectations for wage growth declined significantly.

According to the survey, consumer expectations for interest rates have fallen sharply, although they expect rates to rise over the 1-year to 5-year horizon, albeit moderately. At the same time, expectations for average house price growth have dropped to zero for Canada as a whole. For Ontario, respondents expect the average home price to rise by 1% over the next year. In BC, people see home prices falling a moderate -0.30%, with Albertan respondents suggesting a price decline of -4.3% (see the chart below). It is important to note that oil prices have risen considerably since the completion of this survey. All of these forecasts are well below the figures in the Q1 study.

It is noteworthy that all of these expectations are well below the CMHC forecast for the national average home price to fall 9%-to-18% over the coming year.

This article was written by DLC's chief economist Dr Sherry Cooper.

RECENT POSTS

Your credit score is one of the most important numbers in your financial life — especially when it comes to getting a mortgage. But for most Canadians, how that number actually gets calculated remains a bit of a mystery.

Did you know there’s a program that allows you to use your RRSP to help come up with your downpayment to buy a home? It’s called the Home Buyer’s Plan (or HBP for short), and it’s made possible by the government of Canada. While the program is pretty straightforward, there are a few things you need to know. Your first home (with some exceptions) To qualify, you need to be buying your first home. However, when you look into the fine print, you find that technically, you must not have owned a home in the last four years or have lived in a house that your spouse owned in the previous four years. Another exception is for those with a disability or those helping someone with a disability. In this case, you can withdraw from an RRSP for a home purchase at any time. You have to pay back the RRSP You have 15 years to pay back the RRSP, and you start the second year after the withdrawal. While you won’t pay any tax on this particular withdrawal, it does come with some conditions. You’ll have to pay back the total amount you withdrew over 15 years. The CRA will send you an HBP Statement of Account every year to advise how much you owe the RRSP that year. Your repayments will not count as contributions as you’ve already received the tax break from those funds. Access to funds The funds you withdraw from the RRSP must have been there for at least 90 days. You can still technically withdraw the money from your RRSP and use it for your down-payment, but it won’t be tax-deductible and won’t be part of the HBP. You can access up to $35,000 individually or $70,00 per couple through the HBP. Please connect anytime if you’d like to know more about the HBP and how it could work for you as you plan your downpayment. It would be a pleasure to work with you.