The Canadian Housing Market | March 2020

DLC Canadian Mortgage Experts • March 16, 2020

An assessment of the Canadian housing market by Dr. Sherry Cooper.

The Canadian Real Estate Association announced this morning that home sales recorded over the Canadian MLS Systems rose 5.9% in February, marking one of the more substantial month-over-month gains of the past decade. Actual (not seasonally adjusted) sales activity stood 26.9% above year-ago levels--keeping in mind that activity was quite weak one year ago. February 2019 marked a decade-low for the month, so a good part of the significant y-o-y gain reflects low levels of activity recorded at the time. February 2020 also benefited from an additional day due to the leap year.

The CREA President, Jason Stephen, said, "Home prices are accelerating in markets where listings are in increasingly short supply, specifically in Ontario, Quebec and the Maritimes which together account for about two-thirds of national sales activity. Meanwhile, ample supply across the Prairies and in Newfoundland and Labrador means increased competition among sellers."

The number of newly listed homes jumped 7.3% in February compared to January, more than erasing the declines of late last year. New supply gains were posted in some large markets, including the Fraser Valley, Calgary, Edmonton, the GTA, Hamilton-Burlington, Kitchener-Waterloo, Windsor-Essex, Ottawa and Montreal.

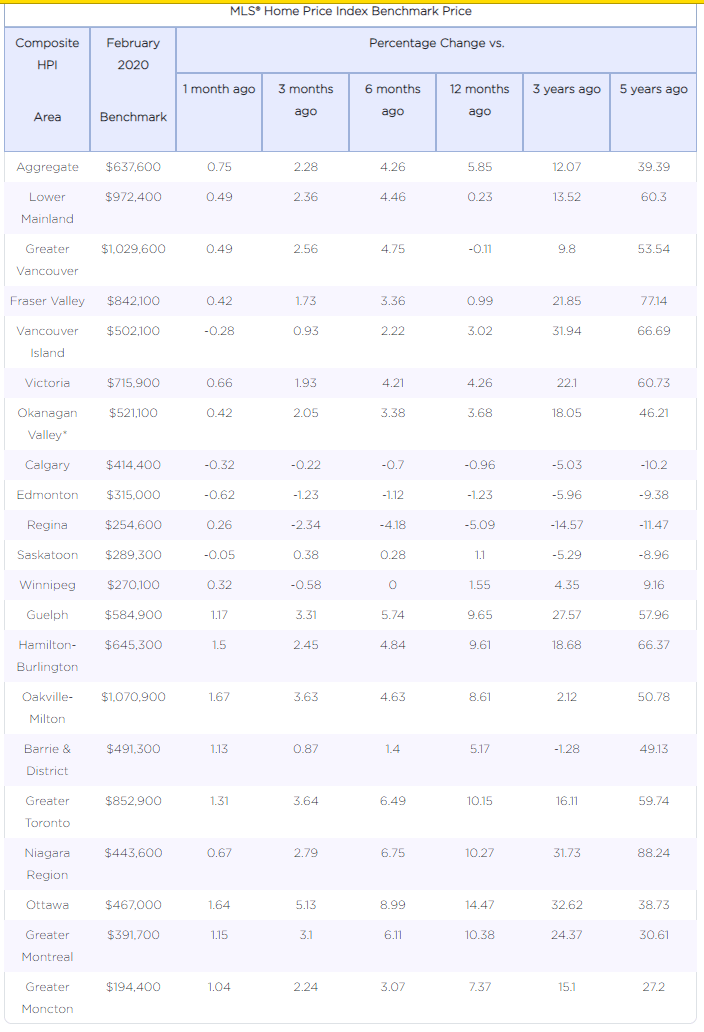

The Aggregate Composite MLS® Home Price Index (MLS® HPI) rose 0.7% in February 2020 compared to January, marking its ninth consecutive monthly gain. The actual (not seasonally adjusted) national average price for homes sold in February 2020 was around $540,000, up 15.2% from the same month the previous year. See the table below for the regional move in prices.

But this is old news, particularly given all that has happened in the past two weeks. What comes next for the housing market? That depends on the course of the pandemic. Lower interest rates would typically be great news for the housing market, particularly for first-time homebuyers. But social distancing is hardly consistent with open houses and home shopping.

The CREA President, Jason Stephen, said, "Home prices are accelerating in markets where listings are in increasingly short supply, specifically in Ontario, Quebec and the Maritimes which together account for about two-thirds of national sales activity. Meanwhile, ample supply across the Prairies and in Newfoundland and Labrador means increased competition among sellers."

The number of newly listed homes jumped 7.3% in February compared to January, more than erasing the declines of late last year. New supply gains were posted in some large markets, including the Fraser Valley, Calgary, Edmonton, the GTA, Hamilton-Burlington, Kitchener-Waterloo, Windsor-Essex, Ottawa and Montreal.

The Aggregate Composite MLS® Home Price Index (MLS® HPI) rose 0.7% in February 2020 compared to January, marking its ninth consecutive monthly gain. The actual (not seasonally adjusted) national average price for homes sold in February 2020 was around $540,000, up 15.2% from the same month the previous year. See the table below for the regional move in prices.

But this is old news, particularly given all that has happened in the past two weeks. What comes next for the housing market? That depends on the course of the pandemic. Lower interest rates would typically be great news for the housing market, particularly for first-time homebuyers. But social distancing is hardly consistent with open houses and home shopping.

Moreover, volatility and instability reduce consumer confidence. Buyers that parked their downpayment savings in the stock markets have lost nearly a third of their money on paper. And how many sellers want a trail of strangers wandering through their homes during the pandemic. So the housing market, like everything else, is likely going to slow over the near term.

The Bank of Canada is hopeful that its rate cuts will stabilize the housing market from what might have otherwise been a substantial shutdown. Lower rates will filter through to lower monthly payments for floating-rate mortgage borrowers. Expect the Bank to cut rates again to near-zero levels, following in the footsteps of the Fed. So far, as of this writing, the Canadian banks have not responded to Friday's BoC rate cut. The prime rate went down a full 50 bps on March 5 after the Bank cut its key rate by that amount on March 4. But so far, the Big-Six banks have not responded to the 75 bps cut three days ago.

The Bank of Canada is hopeful that its rate cuts will stabilize the housing market from what might have otherwise been a substantial shutdown. Lower rates will filter through to lower monthly payments for floating-rate mortgage borrowers. Expect the Bank to cut rates again to near-zero levels, following in the footsteps of the Fed. So far, as of this writing, the Canadian banks have not responded to Friday's BoC rate cut. The prime rate went down a full 50 bps on March 5 after the Bank cut its key rate by that amount on March 4. But so far, the Big-Six banks have not responded to the 75 bps cut three days ago.

This article was written by Dr. Sherry Cooper, DLC's Chief Economist

RECENT POSTS

Your credit score is one of the most important numbers in your financial life — especially when it comes to getting a mortgage. But for most Canadians, how that number actually gets calculated remains a bit of a mystery.

Did you know there’s a program that allows you to use your RRSP to help come up with your downpayment to buy a home? It’s called the Home Buyer’s Plan (or HBP for short), and it’s made possible by the government of Canada. While the program is pretty straightforward, there are a few things you need to know. Your first home (with some exceptions) To qualify, you need to be buying your first home. However, when you look into the fine print, you find that technically, you must not have owned a home in the last four years or have lived in a house that your spouse owned in the previous four years. Another exception is for those with a disability or those helping someone with a disability. In this case, you can withdraw from an RRSP for a home purchase at any time. You have to pay back the RRSP You have 15 years to pay back the RRSP, and you start the second year after the withdrawal. While you won’t pay any tax on this particular withdrawal, it does come with some conditions. You’ll have to pay back the total amount you withdrew over 15 years. The CRA will send you an HBP Statement of Account every year to advise how much you owe the RRSP that year. Your repayments will not count as contributions as you’ve already received the tax break from those funds. Access to funds The funds you withdraw from the RRSP must have been there for at least 90 days. You can still technically withdraw the money from your RRSP and use it for your down-payment, but it won’t be tax-deductible and won’t be part of the HBP. You can access up to $35,000 individually or $70,00 per couple through the HBP. Please connect anytime if you’d like to know more about the HBP and how it could work for you as you plan your downpayment. It would be a pleasure to work with you.