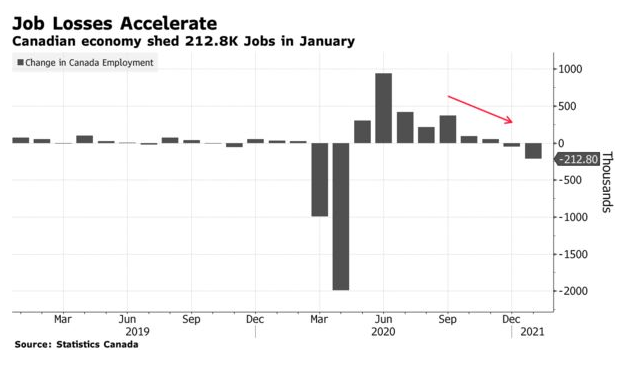

Canadian Employment Falls to Lowest Level Since August

Extended Lockdowns Batter Jobs Market

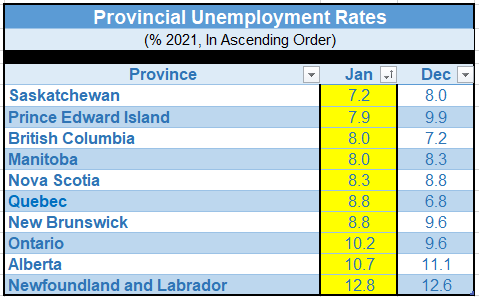

The employment losses were entirely in the two provinces that had the toughest restrictions—Ontario and Quebec—as jobs rose in 7 of the 10 provinces. The table below shows the jobless rate fell in Alberta, New Brunswick, Nova Scotia, Manitoba, PEI and Saskatchewan.

Bottom Line

With the decline in COVID cases in recent weeks, there is some hope that restrictions will be eased. Quebec has already announced it will start to loosen some restrictions on gyms, restaurants and bars in the coming days, and Ontario is on pace to reopen more schools. However, public health officials warn that new variants of the virus remain a risk and urge for continued lockdowns.

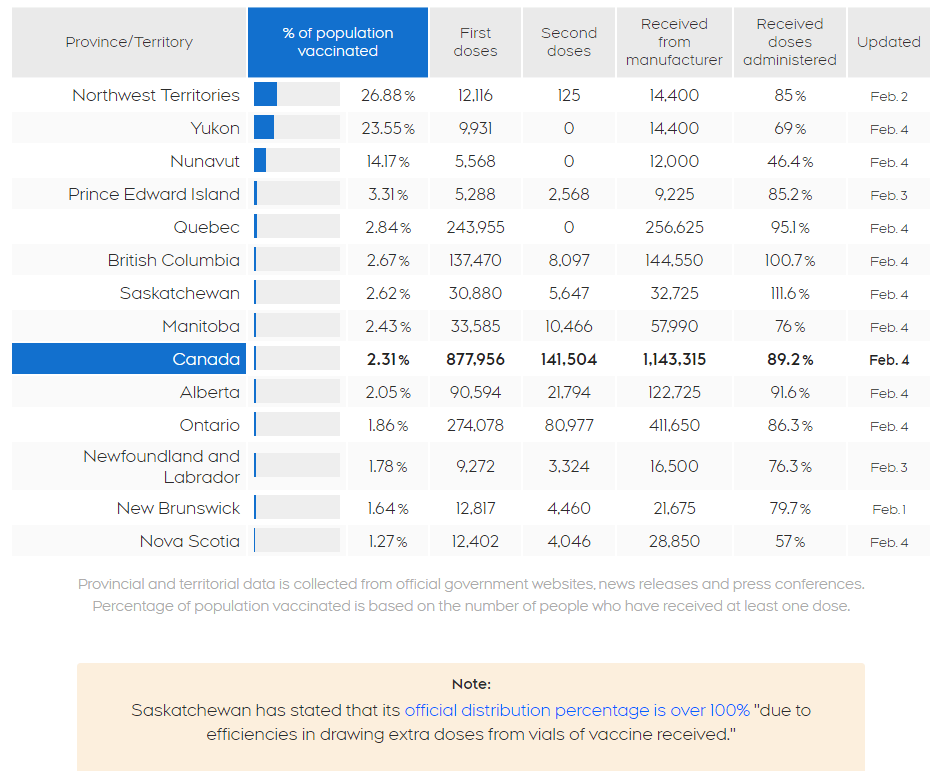

There is no question that the bright light at the end of the very dark pandemic tunnel is a widely distributed vaccine. On that score, Canada is faring badly. The Biden administration is working hard to step-up vaccine distribution, but Canada apparently placed its vaccine orders well after the US and UK. Production issues have harshly slowed Canada’s supply of vaccines. While the US and UK have already broadened distribution to all people aged 65 and over, Canada hasn’t even finished vaccinating health care workers and long-term care residents. Reports suggest that significantly more supply will not be forthcoming until April.

The chart below describes the Canadian vaccine rollout. We now rank 34th in the world in terms of total vaccination doses administered per 100 people.

This article was written by DLC's Chief Economist Dr Sherry Cooper and was syndicated with permission.