Weakest Canadian Employment Report in a Decade

Jackson Middleton • December 9, 2019

Shockingly weak jobs report in November on the heels of tepid report in October. Will BoC rethink its stance?

Huge Decline in Jobs in November As Jobless Rate Surges

One month does not a trend make. Statistics Canada announced this morning that the country lost 71,200 jobs in November , the worst performance in a decade. What's more, the details of the jobs report are no better than the headline. Full-time employment was down 38.4k, and the private sector shed 50.2k. The jobless rate also rose sharply, up four ticks (the most significant monthly jump since the recession), to 5.9%. Hours worked fell 0.3%, and remain an area of persistent disappointment—they’re now up just 0.25% y/y, much more muted than the 1.6% annual job gain.

The one

area of strength was wages

, with growth accelerating to match a cycle high at 4.5% y/y. But wages tend to lag the labour market cycle, so if this weakness is the start of something bigger, wages gains are likely to slow.

The monthly moves were soft, no matter how you slice them. Both full-time (-38.4k) and part-time employment (-32.8k) were down. Similarly, private sector employment (-50.2k) led the way, but self-employment (-18.7k) and the public sector (-2.3k) also saw net losses.

Until last month, we saw a long string of robust job reports in what is usually a very volatile data series, so a correction is not surprising. But this report appears to be more than a statistical quirk and belies the Bank of Canada's statements this week that the Canadian economy remains resilient. Employment is still up 26k per month in 2019 to date consistent with a 1.6% y/y gain, and most of that comes from full-time work. And some of the drop in November reflected a decline in public administration jobs retracing October's gain that might have been related to the federal election. Nevertheless, the 0.4 percentage point uptick in the jobless rate is the largest since the financial crisis in early 2009, and manufacturing jobs were down more than 50k over the past two months.

By industry, job declines were widespread in the month, with only 5 of 16 major sectors posting improvement. Net losses were shared across both the goods and service sectors. Manufacturing (-27.5k) shed jobs for a second month, and notable declines were seen in public administration (-24.9k, likely a reflection of post-election adjustment) and accommodation and food services (-11k).

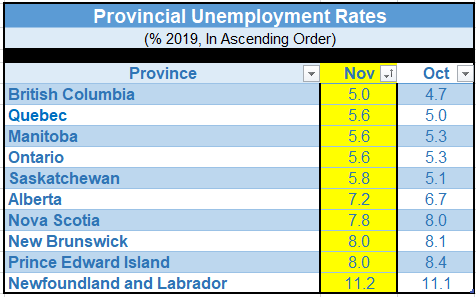

By region, Ontario and PEI were the only provinces to manage job growth last month, with all others deeply in the red. Quebec stands out, shedding 45.1k net positions in a second monthly employment decline and pushing the unemployment up to 5.6% (from 5.0%; the largest monthly increase in nearly eight years). Quebec's jobless rate is now equivalent to that in Ontario. Things were not much better out west: Alberta and B.C. both lost 18.2k net positions. In the case of the former, this was enough to send the unemployment rate up half a point, to 7.2%. Ontario bucked the trend, adding 15.4k net positions, just shy of erasing the prior month's drop. Still, the unemployment rate in the province rose to 5.3% (from 5.0%), as more people joined the labour force. (See the table below.)

Job growth slowed in the second half of this year. Over that period, the average monthly job gain has been a paltry 5.9k compared to an average monthly gain of 24.4k over the past year. For private sector employment, the equivalent figure flipped into negative territory (-4.3k) for the first time in more than a year.

Bottom Line : Today's report means that the Bank of Canada will be keeping an even more watchful eye on the jobs report. The year-on-year pace of net hiring has decelerated for three straight months now, driven in large part by a slowing pace of private-sector hiring. It seems a safe bet that even if we see some recovery in the coming months, the substantial gains of recent years are unlikely to be repeated.

The Bank of Canada has been emphasizing Canada's economic resilience in its recent communications. One month of soft jobs data will hardly break that narrative, but coming after a modest October, it is not hard to imagine a hair more worry about the durability of growth. The bigger question is whether this weakness persists, and more importantly if it feeds into consumer spending behaviour and housing activity, the Bank's key bellwethers.

We continue to believe that the BoC will cut rates in 2020, owing mainly to Canada's vulnerability to trade uncertainty. The loonie sold off sharply on the employment news, particularly so because of the stronger-than-expected labour market report released this morning in the US.

The monthly moves were soft, no matter how you slice them. Both full-time (-38.4k) and part-time employment (-32.8k) were down. Similarly, private sector employment (-50.2k) led the way, but self-employment (-18.7k) and the public sector (-2.3k) also saw net losses.

Until last month, we saw a long string of robust job reports in what is usually a very volatile data series, so a correction is not surprising. But this report appears to be more than a statistical quirk and belies the Bank of Canada's statements this week that the Canadian economy remains resilient. Employment is still up 26k per month in 2019 to date consistent with a 1.6% y/y gain, and most of that comes from full-time work. And some of the drop in November reflected a decline in public administration jobs retracing October's gain that might have been related to the federal election. Nevertheless, the 0.4 percentage point uptick in the jobless rate is the largest since the financial crisis in early 2009, and manufacturing jobs were down more than 50k over the past two months.

By industry, job declines were widespread in the month, with only 5 of 16 major sectors posting improvement. Net losses were shared across both the goods and service sectors. Manufacturing (-27.5k) shed jobs for a second month, and notable declines were seen in public administration (-24.9k, likely a reflection of post-election adjustment) and accommodation and food services (-11k).

By region, Ontario and PEI were the only provinces to manage job growth last month, with all others deeply in the red. Quebec stands out, shedding 45.1k net positions in a second monthly employment decline and pushing the unemployment up to 5.6% (from 5.0%; the largest monthly increase in nearly eight years). Quebec's jobless rate is now equivalent to that in Ontario. Things were not much better out west: Alberta and B.C. both lost 18.2k net positions. In the case of the former, this was enough to send the unemployment rate up half a point, to 7.2%. Ontario bucked the trend, adding 15.4k net positions, just shy of erasing the prior month's drop. Still, the unemployment rate in the province rose to 5.3% (from 5.0%), as more people joined the labour force. (See the table below.)

Job growth slowed in the second half of this year. Over that period, the average monthly job gain has been a paltry 5.9k compared to an average monthly gain of 24.4k over the past year. For private sector employment, the equivalent figure flipped into negative territory (-4.3k) for the first time in more than a year.

Bottom Line : Today's report means that the Bank of Canada will be keeping an even more watchful eye on the jobs report. The year-on-year pace of net hiring has decelerated for three straight months now, driven in large part by a slowing pace of private-sector hiring. It seems a safe bet that even if we see some recovery in the coming months, the substantial gains of recent years are unlikely to be repeated.

The Bank of Canada has been emphasizing Canada's economic resilience in its recent communications. One month of soft jobs data will hardly break that narrative, but coming after a modest October, it is not hard to imagine a hair more worry about the durability of growth. The bigger question is whether this weakness persists, and more importantly if it feeds into consumer spending behaviour and housing activity, the Bank's key bellwethers.

We continue to believe that the BoC will cut rates in 2020, owing mainly to Canada's vulnerability to trade uncertainty. The loonie sold off sharply on the employment news, particularly so because of the stronger-than-expected labour market report released this morning in the US.

In October, employment increased in British Columbia and Newfoundland and Labrador and was little changed in the other provinces. Employment declined in manufacturing and construction. At the same time, net new jobs were up in public administration and finance, insurance, real estate, rental and leasing. The number of self-employed workers decreased, while the number of employees in the public sector increased for the second consecutive month.

This article was written by DLC's Chief Economist Dr. Sherry Cooper, it was originally included in her subscriber email list and published with permission.

RECENT POSTS

Your credit score is one of the most important numbers in your financial life — especially when it comes to getting a mortgage. But for most Canadians, how that number actually gets calculated remains a bit of a mystery.

Did you know there’s a program that allows you to use your RRSP to help come up with your downpayment to buy a home? It’s called the Home Buyer’s Plan (or HBP for short), and it’s made possible by the government of Canada. While the program is pretty straightforward, there are a few things you need to know. Your first home (with some exceptions) To qualify, you need to be buying your first home. However, when you look into the fine print, you find that technically, you must not have owned a home in the last four years or have lived in a house that your spouse owned in the previous four years. Another exception is for those with a disability or those helping someone with a disability. In this case, you can withdraw from an RRSP for a home purchase at any time. You have to pay back the RRSP You have 15 years to pay back the RRSP, and you start the second year after the withdrawal. While you won’t pay any tax on this particular withdrawal, it does come with some conditions. You’ll have to pay back the total amount you withdrew over 15 years. The CRA will send you an HBP Statement of Account every year to advise how much you owe the RRSP that year. Your repayments will not count as contributions as you’ve already received the tax break from those funds. Access to funds The funds you withdraw from the RRSP must have been there for at least 90 days. You can still technically withdraw the money from your RRSP and use it for your down-payment, but it won’t be tax-deductible and won’t be part of the HBP. You can access up to $35,000 individually or $70,00 per couple through the HBP. Please connect anytime if you’d like to know more about the HBP and how it could work for you as you plan your downpayment. It would be a pleasure to work with you.