Surprisingly Strong Canadian Jobs Report in May

Jackson Middleton • June 7, 2019

Another Strong Employment Report Signals Rebound In Canadian Economy

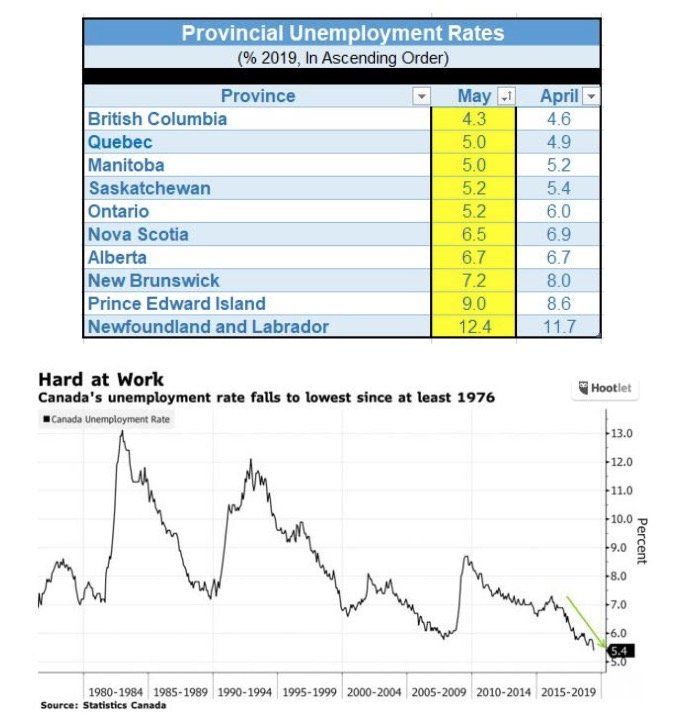

It appears that the Bank of Canada's optimism that the Canadian economy's growth will pick up in the third and fourth quarters of this year is well founded. Not only was the employment report very robust for two consecutive months, but the jobless rate has fallen to its lowest level since at least 1976.

Also, Canada's trade deficit, reported today, hit a six-month low in April, as exports continue to rebound from a recent slump. Consumer spending and business investment are also making a big comeback. Household spending has accelerated, despite concerns over bloated debt loads, assisted by easing rates on loans, substantial jobs gains, stabilizing housing markets and improving financial markets.

The Bank of Canada forecasts that growth will accelerate to an annualized 1.3% in the second quarter--following the meagre 0.4% expansion in Q1--and pick up further in the second half of this year, before accelerating back to above 2% growth by 2020. This comeback begs the question--why were markets expecting a rate cut by the bank in December? That expectation may well change after this morning's Statistics Canada releases. Of course, one caveat remains, which is the uncertainty surrounding a trade war with China and Mexico. If the trade situation were to worsen, Canada's economy would undoubtedly be sideswiped.

Canadian employment rose by 27,700 in May, bring the number of jobs created over the past year to a whopping 453,100. The jobless rate plunged to 5.4%, from 5.7% in April, the lowest in data going back to 1976. Economists had been forecasting employment to rise by only 5,000 last month after Canada recorded a record gain of 106,500 in April. The loonie jumped on the news.

The composition of the job gain was particularly heartening, as the rise was all in full-time employment. On the other hand, jobs by those who are self-employed increased by 61,500--the gig economy is alive and well.

The Bank of Canada forecasts that growth will accelerate to an annualized 1.3% in the second quarter--following the meagre 0.4% expansion in Q1--and pick up further in the second half of this year, before accelerating back to above 2% growth by 2020. This comeback begs the question--why were markets expecting a rate cut by the bank in December? That expectation may well change after this morning's Statistics Canada releases. Of course, one caveat remains, which is the uncertainty surrounding a trade war with China and Mexico. If the trade situation were to worsen, Canada's economy would undoubtedly be sideswiped.

Canadian employment rose by 27,700 in May, bring the number of jobs created over the past year to a whopping 453,100. The jobless rate plunged to 5.4%, from 5.7% in April, the lowest in data going back to 1976. Economists had been forecasting employment to rise by only 5,000 last month after Canada recorded a record gain of 106,500 in April. The loonie jumped on the news.

The composition of the job gain was particularly heartening, as the rise was all in full-time employment. On the other hand, jobs by those who are self-employed increased by 61,500--the gig economy is alive and well.

The most substantial job gains were in Ontario and BC.

Wage growth continued to be strong in May as pay gains for permanent workers sere steady at 2.6%.

In direct contrast, the US jobs report, also released today, was weaker than expected. US payrolls and wage gains cooled as Trump's trade war weighed on the economy. US employers added the fewest workers in three months, and wage gains eased, suggesting broader economic weakness and boosting expectations for a Federal Reserve interest-rate cut as President Donald Trump’s trade policies weigh on growth.

Wage growth continued to be strong in May as pay gains for permanent workers sere steady at 2.6%.

In direct contrast, the US jobs report, also released today, was weaker than expected. US payrolls and wage gains cooled as Trump's trade war weighed on the economy. US employers added the fewest workers in three months, and wage gains eased, suggesting broader economic weakness and boosting expectations for a Federal Reserve interest-rate cut as President Donald Trump’s trade policies weigh on growth.

This article was written by DLC's Chief Economist Dr. Sherry Cooper and included in her regular newsletter.

RECENT POSTS

Your credit score is one of the most important numbers in your financial life — especially when it comes to getting a mortgage. But for most Canadians, how that number actually gets calculated remains a bit of a mystery.

Did you know there’s a program that allows you to use your RRSP to help come up with your downpayment to buy a home? It’s called the Home Buyer’s Plan (or HBP for short), and it’s made possible by the government of Canada. While the program is pretty straightforward, there are a few things you need to know. Your first home (with some exceptions) To qualify, you need to be buying your first home. However, when you look into the fine print, you find that technically, you must not have owned a home in the last four years or have lived in a house that your spouse owned in the previous four years. Another exception is for those with a disability or those helping someone with a disability. In this case, you can withdraw from an RRSP for a home purchase at any time. You have to pay back the RRSP You have 15 years to pay back the RRSP, and you start the second year after the withdrawal. While you won’t pay any tax on this particular withdrawal, it does come with some conditions. You’ll have to pay back the total amount you withdrew over 15 years. The CRA will send you an HBP Statement of Account every year to advise how much you owe the RRSP that year. Your repayments will not count as contributions as you’ve already received the tax break from those funds. Access to funds The funds you withdraw from the RRSP must have been there for at least 90 days. You can still technically withdraw the money from your RRSP and use it for your down-payment, but it won’t be tax-deductible and won’t be part of the HBP. You can access up to $35,000 individually or $70,00 per couple through the HBP. Please connect anytime if you’d like to know more about the HBP and how it could work for you as you plan your downpayment. It would be a pleasure to work with you.