Interest Rates & Commodity Prices Surge On Economic Rebound Optimism

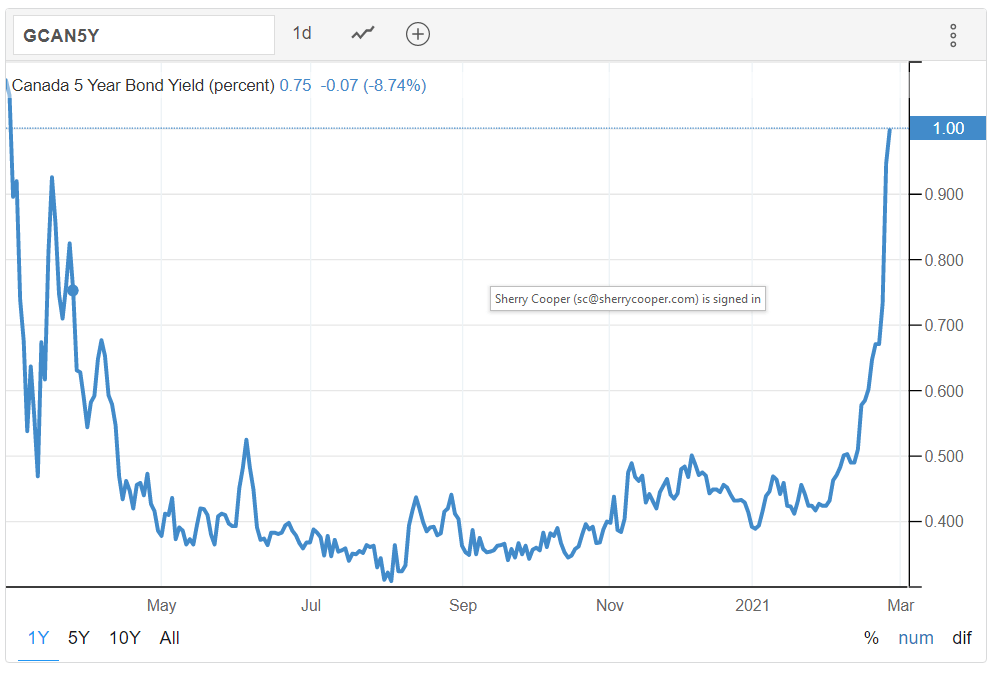

Canadian 5-Year Bond Yield Surges

Keep in mind that Canada’s economy has considerable slack with unemployment rising in recent months and the lockdown continuing for at least a couple more weeks in the GTA. Moreover, Canada has fallen far behind other countries in the vaccine rollout. But there is no denying that pent-up demand in Canada is high. Not only have home sales been breaking records, but auto sales and anything housing-related–such as Home Depot earning growth–have skyrocketed.

Savings rates are high, and the big banks have reported a surge in deposit growth as consumers squirrel away those savings. Remember, the Roaring Twenties was a response to the 1918 Pandemic, more than anything else.

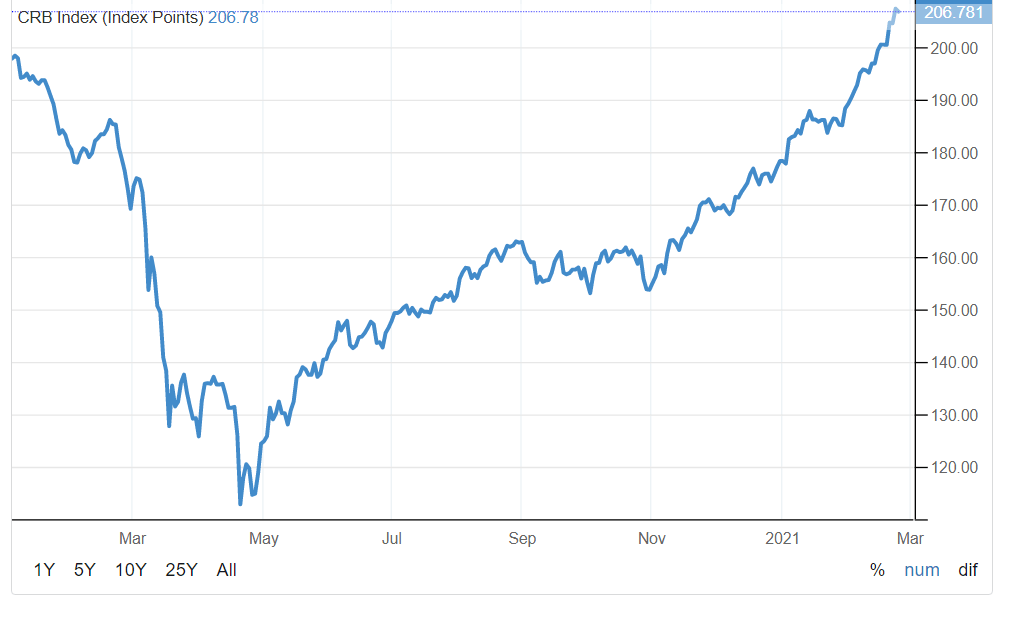

The CRB commodity price index, shown below, is on a tear, and the gains are in every sector except gold and orange juice. That means that new home construction costs are also rising, as home sales remain well above listings.

Bottom Line

It’s time to lock-in mortgage rates. For those in the market, preapprovals are prudent. Rising rates will likely trigger more housing activity in the near-term as those thinking of buying might move off the sidelines, pushing prices higher over the first half of this year.

The surge in interest rates would undoubtedly stall or reverse if we see a third wave of new variant COVID cases in advance of a full rollout of the vaccines in Canada. However, there is enough monetary and fiscal stimulus in global markets, and oil prices are expected to continue to rally sufficiently that an ultimate rise in interest rates cannot be far off. This is indicated by the loonie moving to a near a 3-year high.

This article was written by DLC's Chief Economist Dr Sherry Cooper and was syndicated with permission.