Housing Market Slowed in April as Renewed Lockdown Took Its Toll

Starting to See A Slowdown In Canadian Housing

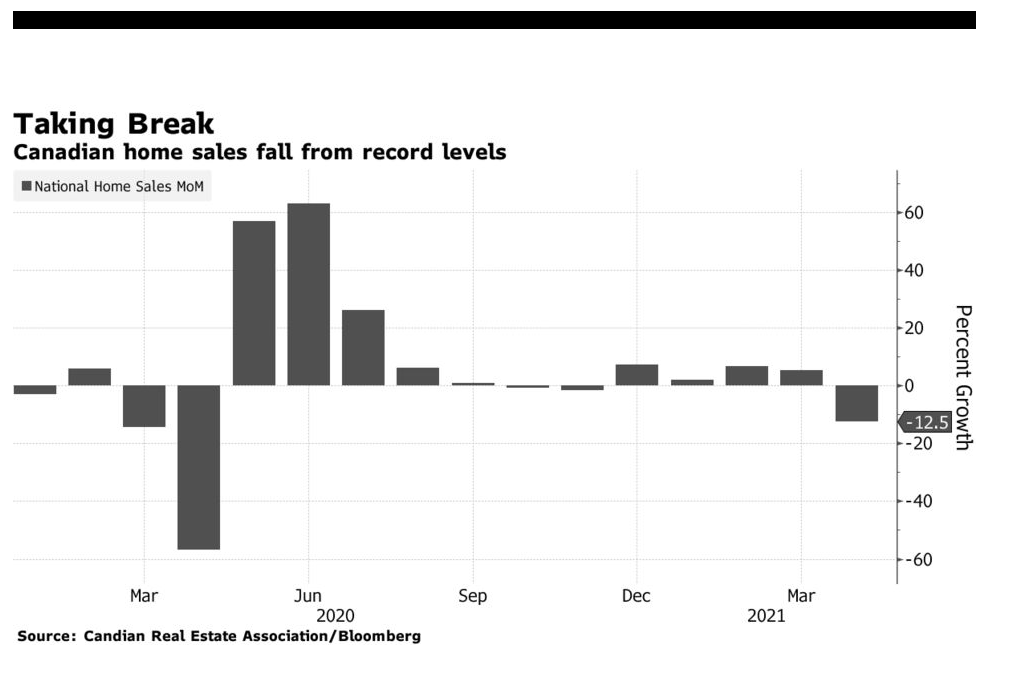

Today, the Canadian Real Estate Association (CREA) released statistics showing national existing home sales fell 12.4% nationally from March to April 2021. Over the same period, the number of newly listed properties fell 5.4%, and the MLS Home Price Index rose 2.4%.

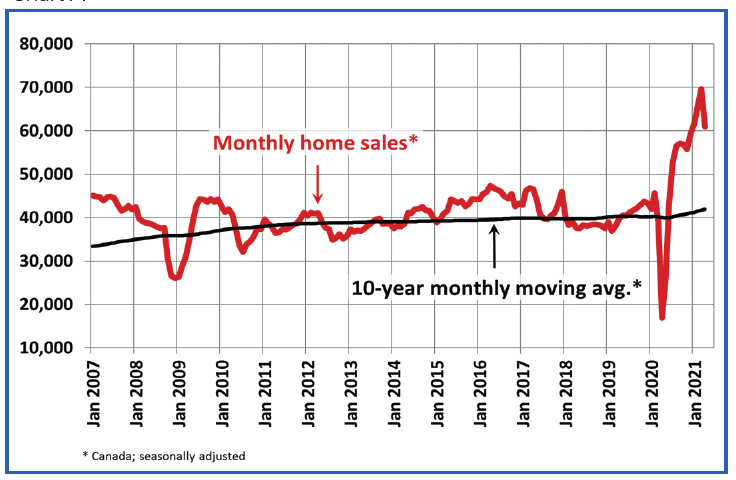

While home sales fell month-over-month in April, largely due to the new lockdowns, April sales were still the strongest ever for that month and well above the 10-year monthly average.

Month-over-month declines in sales activity were observed in close to 85% of all local markets, including virtually all of B.C. and Ontario.

New Listings

The number of newly listed homes declined by 5.4% in April compared to March. In a market with historically low inventory, where sales activity depends on a steady supply of new listings each month, the synchronous gains in new supply and sales in March followed by synchronous declines in April suggest the slowdown in sales may be partially about the availability of listings as opposed to only a demand story. New listings were down in 70% of all local markets in April.

The national sales-to-new listings ratio eased back to 75.2% in April compared to a peak level of 90.6% back in January. That said, the long-term average for the national sales-to-new listings ratio is 54.5%, so it is currently still high historically. The good news is that it is moving in the right direction.

Based on a comparison of sales-to-new listings ratio with long-term averages, only about a quarter of all local markets were in balanced market territory in April, measured as being within one standard deviation of their long-term average. The other three-quarters of markets were above long-term norms, in many cases well above.

There were 2 months of inventory on a national basis at the end of April 2021, up from a record-low 1.7 months in March but still well below the long-term average for this measure of a little more than 5 months.

In a separate release, Canadian housing starts fell to 268,600 annualized units in April from the blowout (334.8k) month in March. While down sharply month-over-month, this is still a solid level of new construction activity in Canada by historical standards. In fact, average annualized starts over the past six months run at the strongest level on record, topping building booms in the 1970s and 1980s. All regions but the Prairies and Atlantic Canada saw lower starts in April.

Home Prices

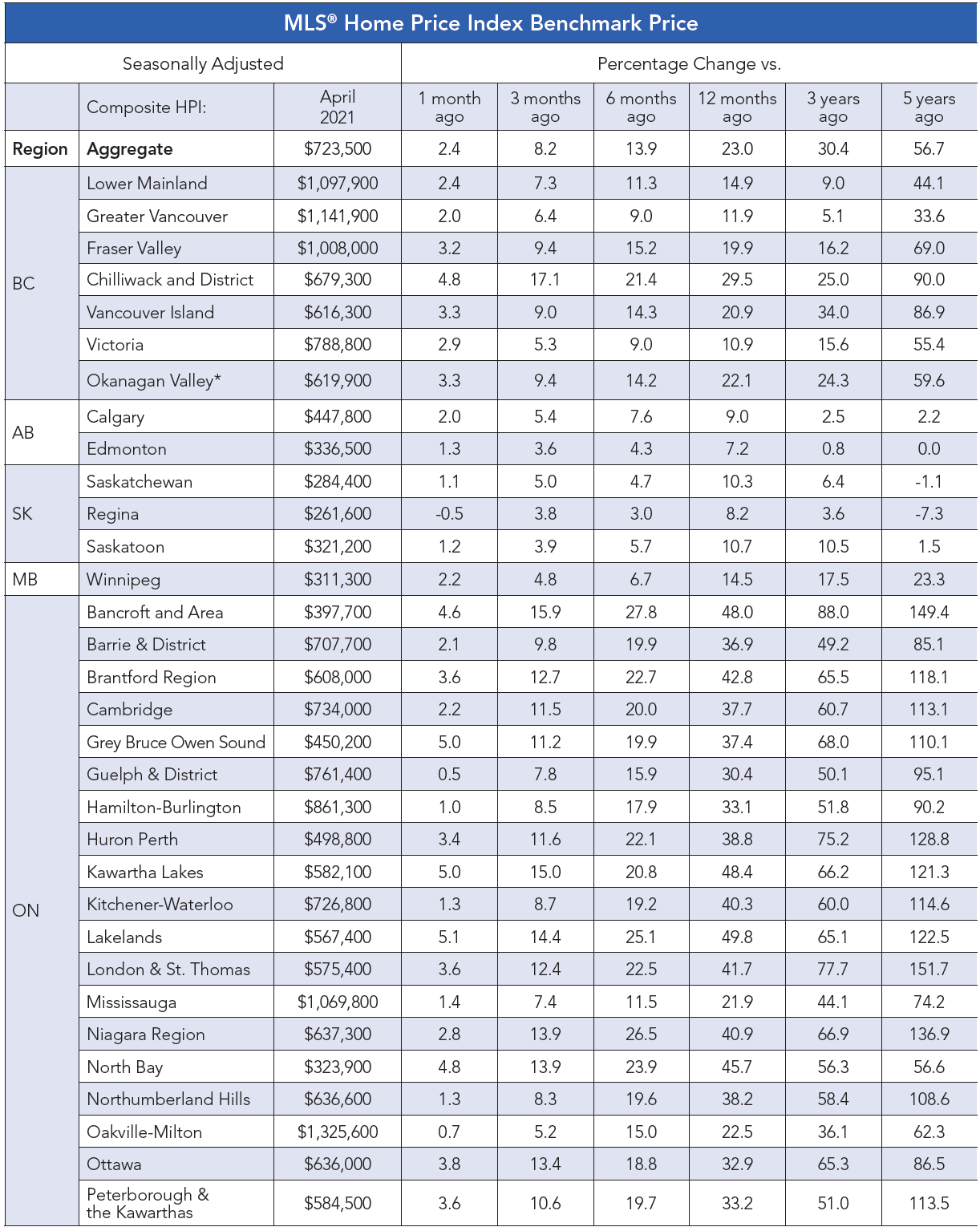

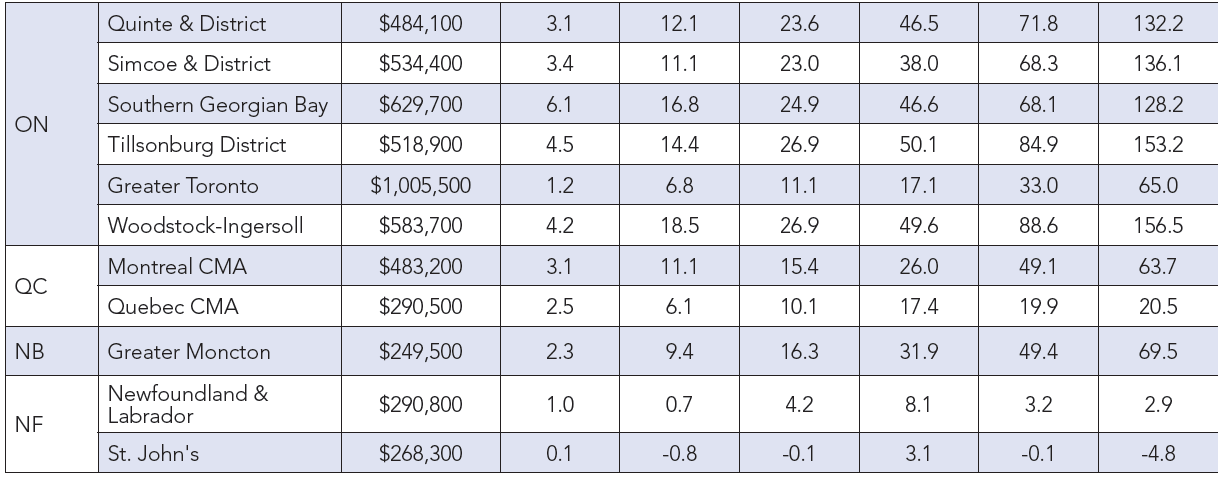

The Aggregate Composite MLS® Home Price Index (MLS® HPI) climbed by 2.4% month-over-month in April 2021 – a historically strong gain but less than in February and March. Most of the recent deceleration in month-over-month price growth has come from the single-family space compared to the more affordable townhome and apartment segments.

The non-seasonally adjusted Aggregate Composite MLS® HPI was up 23.1% on a year-over-year basis in April. Based on data back to 2005, this was a record year-over-year increase.

The largest year-over-year gains continue to be posted across Ontario (around 20-50%), followed by markets in B.C., Quebec and New Brunswick (around 10-30%), and lastly by gains in the Prairie provinces and Newfoundland and Labrador (around 5-15%).

The MLS® HPI provides the best way to gauge price trends because averages are strongly distorted by changes in the mix of sales activity from one month to the next.

The actual (not seasonally adjusted) national average home price was slightly under $696,000 in April 2021, up 41.9% from the same month last year. That said, it is important to remember that the national average price dropped by 10% month-over-month last April as the higher-end of every market effectively shut down for a couple of months. That will serve to stretch these year-over-year comparisons over and above what is actually happening to prices until around June.

By segment: Single-detached remains extremely strong, but earlier signs that condo markets in the large cities were tightening up continue to play out. Condo prices were up 8.5% y/y in April, the strongest pace since mid-2018, and price gains are now running even stronger month-to-month in the biggest cities. We continue to expect these markets to come back stronger than most might think.

By region: It’s as close to wall-to-wall strength that we’ve probably ever seen in this country. Long-dormant markets like Calgary and Edmonton are awake again with prices up roughly 9% y/y; Toronto, Montreal and Vancouver remain strong as usual; some smaller markets (think Halifax, Moncton, Southwestern Ontario) are even stronger than the big cities; and cottage country is booming.

Bottom Line

Headlines will probably flag housing market declines in April, but don’t that fool you…this market is still robust across geography and segment, even if we’ve likely seen peak momentum. Activity will likely remain strong this summer, especially if the COVID restrictions are eased, and people begin to get their second vaccine.

This article was written by DLC's Chief Economist Dr Sherry Cooper and was syndicated with permission.