Half of Canada’s Big Housing Markets Are Unaffordable

A new study of 15 major urban centres across Canada shows that housing un affordability continues to be a major concern in nearly half of those markets.

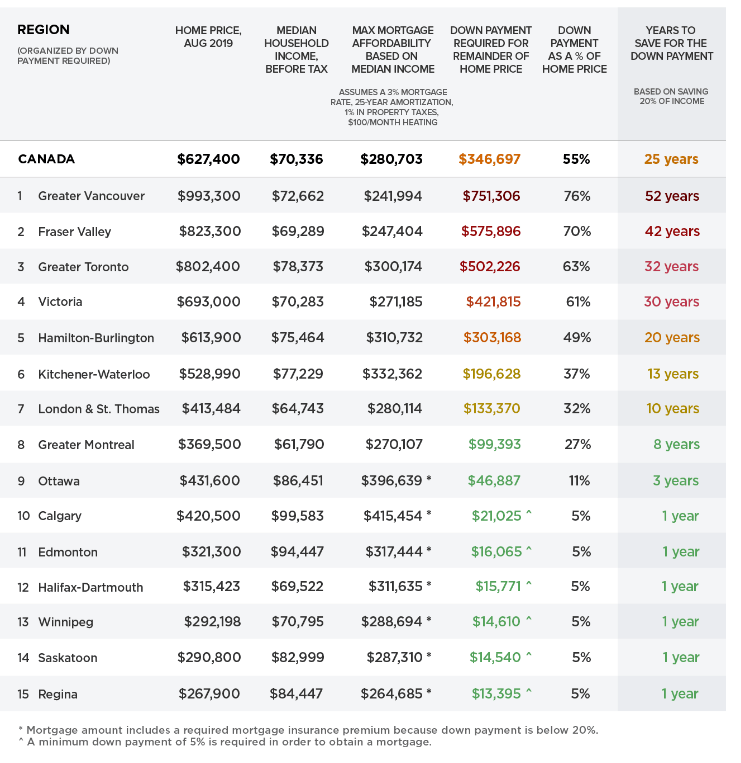

A median-income earner wouldn’t qualify for a mortgage large enough to fund their home purchase in seven key markets, including the Greater Vancouver and Toronto areas, Victoria, Hamilton-Burlington, Kitchener-Waterloo and London-St. Thomas, according to a newly released report from Zoocasa.

Instead, buyers there would need to supplement the mortgage with a “hefty” down payment, the report notes. In Vancouver, for example, a median-income earner making $72,662 would qualify for a mortgage of $241,994 — about $751,300 less than the average home price.

“That would take a household setting aside 20% of their income annually a total of 52 years to save the required funds,” the report notes. Similarly in Toronto, prospective buyers would need to save for 32 years to amass the required down payment.

Zoocasa’s editor-in-chief, Penelope Graham, told the Huffington Post that taking decades to save for a downpayment is “not realistic for anyone, but it’s a way to illustrate what the (affordability) gap is like. We wanted to highlight the median income―just how different market conditions can be across Canada.”

At the other end of the spectrum, the Prairies are home to many of the most affordable markets, including Regina, Saskatoon, Winnipeg and Edmonton.

If you are looking to get into the housing market, but have no idea where to start, please contact any of our Canadian Mortgage Experts anytime, we'd love to walk you through the process!

This article was originally published on the Canadian Mortgage Trendson Sept 29th 2019, written by Steve Huebl.