Canadian Housing Market Very Strong in July

New Listings

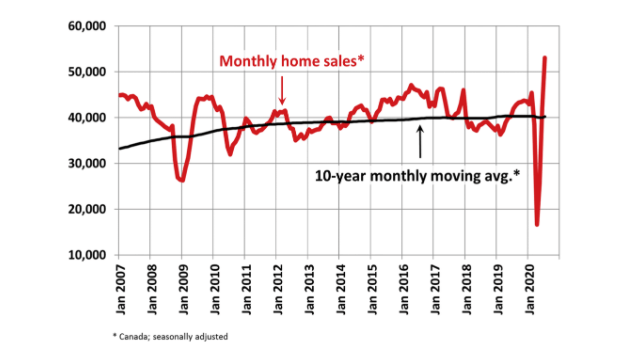

The number of newly listed homes climbed by another 7.6% in July compared to June, to a level of 71,879--the highest level for any July in history. New supply was only up in about 60% of local markets, as the rebound in supply appears to be tapering off in many parts of the country. The national increase in July was dominated by gains in the GTA. More supply is expected to come on the market in future months, particularly once a vaccine is widely available.

With the ongoing rebound in sales activity now far outpacing the recovery in new supply, the national sales-to-new listings ratio tightened to 73.9% in July compared to 63.1% posted in June. It was one of the highest levels on record for this measure, behind just a few months back in late 2001 and early 2002.

Based on a comparison of sales-to-new listings ratios with long-term averages, only about a third of all local markets were in balanced market territory, measured as being within one standard deviation of their long-term average, in July 2020. The other two-thirds of markets were all above long-term norms, in many cases well above.

The number of months of inventory is another important measure of the balance between sales and the supply of listings. It represents how long it would take to liquidate current inventories at the current rate of sales activity.

Housing markets are very tight, especially in Ontario, as demand has far outpaced supply. There were just 2.8 months of inventory on a national basis at the end of July 2020 – the lowest reading on record for this measure. At the local market level, a number of Ontario markets shifted from months of inventory to weeks of inventory in July.

Home Prices

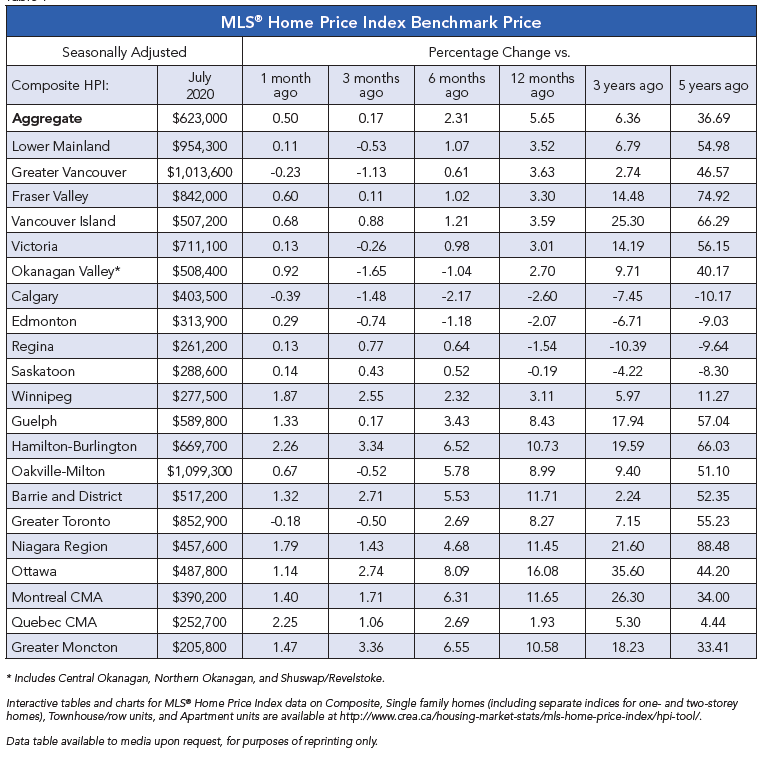

The Aggregate Composite MLS® Home Price Index (MLS® HPI) jumped by 2.3% m-o-m in July 2020 – the second largest increase on record (after March 2017) going back 15 years. (see Table below). Of the 20 markets currently tracked by the index, they all posted m-o-m increases in July.

The biggest m-o-m gains, in the range of 3%, were recorded in the GTA outside of the city of Toronto, Guelph, Ottawa and Montreal; although, generally speaking, most markets east of Saskatchewan are seeing prices accelerate in line with strong sales numbers. Price gains were more modestly positive in B.C. and Alberta.

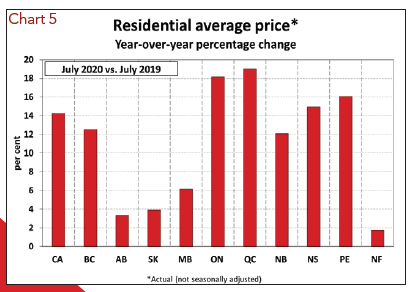

The non-seasonally adjusted Aggregate Composite MLS® HPI was up 7.4% on a y-o-y basis in July the biggest gain since late 2017.

The MLS® HPI provides the best way to gauge price trends because averages are strongly distorted by changes in the mix of sales activity from one month to the next.

The actual (not seasonally adjusted) national average price for homes sold in July 2020 was a record $571,500, up 14.3% from the same month last year.

The national average price is heavily influenced by sales in the Greater Vancouver and the GTA, two of Canada’s most active and expensive housing markets. Excluding these two markets from calculations cuts around $117,000 from the national average price. The extent to which sales continue to fluctuate in these two markets relative to others could have further compositional effects on the national average price, both up and down.

Bottom Line

CMHC has recently forecast that national average sales prices will fall 9%-to-18% in 2020 and not return to yearend-2019 levels until as late as 2022. I continue to believe that this forecast is overly pessimistic. Here we are in the second half of 2020, and the national average sales price has risen 14.3% year-over-year.

The good news is that the housing market is contributing to the recovery in economic activity. While the course of the virus is uncertain, Canada's government has handled the COVID-19 situation very well from both a public health and a fiscal and monetary perspective. The future course of the economy here will depend on the virus. While no one knows what that will be, suffice it to say that Canada's economy is en route to a full recovery, but it may well be a long and bumpy one.