Canada's Fiscal Response To COVID Is The Largest In the Industrialized World

Federal Fiscal Update--Finance Minister Freeland's Debut

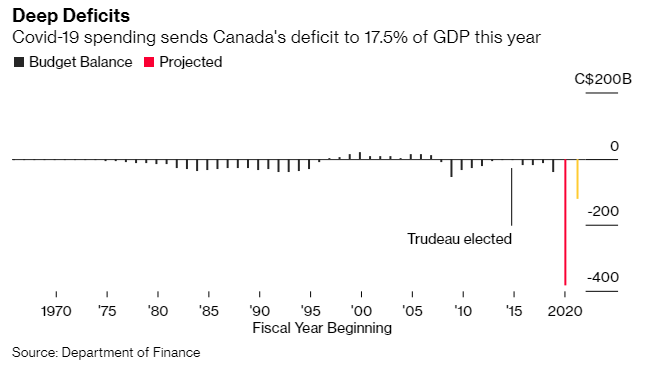

The budgetary red ink is projected at $121 billion next year, before any additional stimulus. In total, spending linked to the government’s COVID response accounted for C$75 billion of this year’s deficit, and C$51 billion next year.

Based on Monday’s projections, the deficit is seen gradually narrowing to about $51 billion in two years and $25 billion by 2025.

The planned stimulus over the next three years will total no more than 4% of GDP, which the document said is in line with the Bank of Canada’s estimate of the level of slack in the economy. Freeland said, “fiscal guardrails” tied to the labour market would help determine the extent of the additional stimulus.

Among the measures announced today, Freeland boosted the government's wage subsidy program (Canada Emergency Wage Subsidy, CEWS) to cover as much as 75% of payroll costs for businesses and extended its commercial rent subsidy and lockdown support top-ups until March. Both were slated to run out on December 20. The current cap on CEWS was 65%.

The federal government plans to create a new funding program to help restaurants, tourism companies and other businesses in industries hardest hit by COVID-19.

The Highly Affected Sectors Credit Availability Program (HASCAP), which was announced in the government’s fiscal update Monday, will offer eligible businesses loans of up to $1 million, with a 10-year term.

The money will be lent by banks or other financial institutions, but guaranteed by the federal government.

“We know that businesses in tourism, hospitality, travel, arts and culture have been particularly hard-hit. So we’re creating a new stream of support for those businesses that need it most — a credit availability program with 100-per-cent government-backed loan support and favourable terms for businesses that have lost revenue as people stay home to fight the spread of the virus,” Finance Minister Chrystia Freeland said in her prepared speech to the House of Commons.

Establishing a national childcare plan is a key long-term goal, with Freeland vowing a detailed plan in next year’s budget. In her forward to the fiscal update, she described the daycare strategy as “a feminist plan” that also “makes sound business sense.”

As a start, the Liberals are proposing in their fiscal update to spend $420 million in grants and bursaries to help provinces and territories train and retain qualified early childhood educators.

The Liberals are also proposing to spend $20 million over five years to build a child-care secretariat to guide federal policy work, plus $15 million in ongoing spending for a similar Indigenous-focused body.

The money is designed to lay the foundation for what will likely be a big-money promise in the coming budget.

Current federal spending on child care expires near the end of the decade, but the Liberals are proposing now to keep the money flowing, starting with $870 million a year in 2028.

There is also money for action on climate change. The government allocated C$2.6 billion in grants for homeowners to improve efficiency and $150 million over three years for electric vehicle charging stations.

The government also detailed some help for the hard-hit tourism sector, including funding for airports. But with Transport Minister Marc Garneau’s negotiations with airlines underway, there is no specific money for carriers including Air Canada and WestJet Airlines Ltd.

Bottom Line

There will continue to be great concern about the largest budget deficits since World War II. Does Canada really need the proportionately largest COVID fiscal response in the industrialized world? The outlook is somewhat less dire than when the government released a fiscal snapshot in July. The unemployment rate at 8.9% is down materially from May’s 13.7% high but well above February’s 5.6%. The economy recovered ground through the third quarter, although the second wave of pandemic and ensuing restrictions undoubtedly will topple economic activity this quarter.

There is little worry that the government can sustain a massive deficit this year. It can, given low debt levels entering the crisis and historically low interest rates. But now that it has no fiscal guardrails, there’s a risk debt-to-GDP will continue to rise in the medium term if it continues to spend ambitiously.

The government is adding a new revenue source by taxing large digital companies. Still, in time, with this level of spending, they will be tempted to raise taxes on domestic sources, for example, hikes in the GST and higher capital gains taxes. This would be misguided, given the fragility of the recovery.

There is a greater risk that the government is overdoing the stimulus with vaccines on the horizon than undergoing it. Canada's programs have been generous and household-focused compared to our G7 peers. The government must be strategic in assuring that new program spending is focused on future growth, beyond the pandemic, so that our debt-to-GDP will resume its downward trend. The risk is that once created; it is difficult to rein in spending.

This article was written by Dr Sherry Cooper, DLC's Chief Economist and was published with permission.