Bank of Canada Raises Rates Cautiously

As was widely expected, the Bank of Canada announced another quarter-point interest rate increase this morning, saying that more hikes are ahead.

The Bank of Canada increased the target overnight interest rate to 1.25%, its highest level since the global financial crisis marking the third rate hike since July. The move comes in the wake of unexpected labour market tightening and strong business confidence and investment. The Canadian economy is bumping up against capacity constraints as the jobless rate has fallen to its lowest level in more than 40 years.

Inflation is just shy of the 2.0% target level and wage rates are rising, albeit at a relatively moderate pace.

Exports have been weaker than expected. NAFTA uncertainty is “weighing increasingly” on Canada’s economic outlook as cross-border shifts in auto production are already beginning.

The MPR goes on to comment that “residential investment is now expected to be roughly flat over the two-year projection horizon. The rate of new household formation is anticipated to support a solid level of housing activity, particularly in the Greater Toronto Area, where the supply of new housing units has not kept pace with demand. However, interest rate increases, as well as macroprudential and other housing policy measures, are expected to weigh on growth in residential investment, since some prospective homebuyers may take on smaller mortgages or delay purchases.”

With higher interest rates, debt-service costs will rise, thus dampening consumption growth, particularly of durable goods, which have been a significant driver of spending in recent quarters. “Elevated levels of household debt are likely to amplify the impact of higher interest rates on consumption, since increased debt-service costs are more likely to constrain some borrowers, forcing them to moderate their expenditures.”

While global oil price benchmarks have risen in the past quarter or so, Canadian oil prices have been flat. Transportation constraints facing Canadian oil producers have held down the price of Western Canada Select oil, leaving it just below October levels. Canadian oil producers have trouble getting oil to the U.S. market, and with no East-West pipelines, they cannot export oil to markets outside of the U.S. This has been a long-standing negative for the Canadian economy.

Markets have been expecting three rate hikes this year, taking the overnight rate to 1.75% by yearend. This level is considerably below the Bank of Canada’s estimate of the so-called neutral overnight rate, which is defined as “the rate consistent with output at its potential level (approximately 1.6%) and inflation equal to the 2.0% target.” For Canada, the neutral benchmark policy rate is estimated to be between 2 .5% and 3 .5%. The need for continued monetary accommodation at full capacity suggests policymakers aren’t anticipating a return to neutral anytime soon.

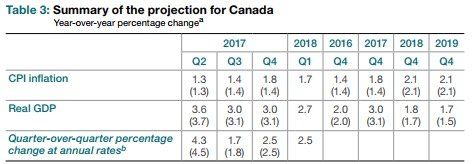

The Bank’s revised forecasts for inflation and real GDP growth are in the following table. The numbers in parentheses are from the projection in the October Monetary Policy Report. Today’s MPR forecasts that inflation will edge upward while economic growth slows from the rapid 2017 pace (3.0%) to levels more consistent with long-term potential (1.7% to 1.8%).

The Bank of Canada’s future actions will continue to be data dependent. The next policy announcement is on March 7 .

This article was written by Dr. Sherry Cooper DLC Chief Economist. It originally appeared here.