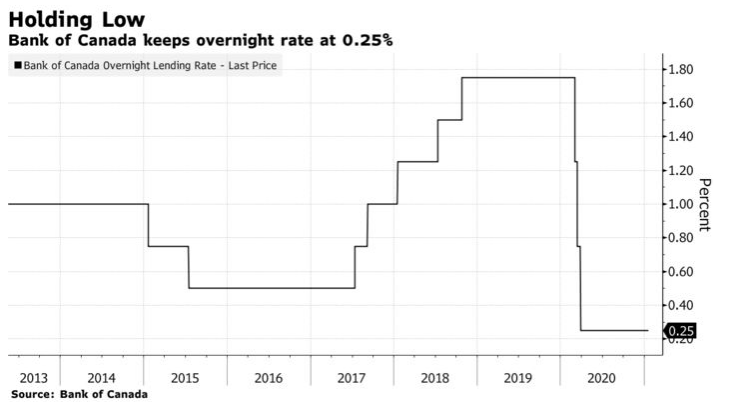

Bank of Canada Expects to Hold Overnight Rates Steady Until 2023

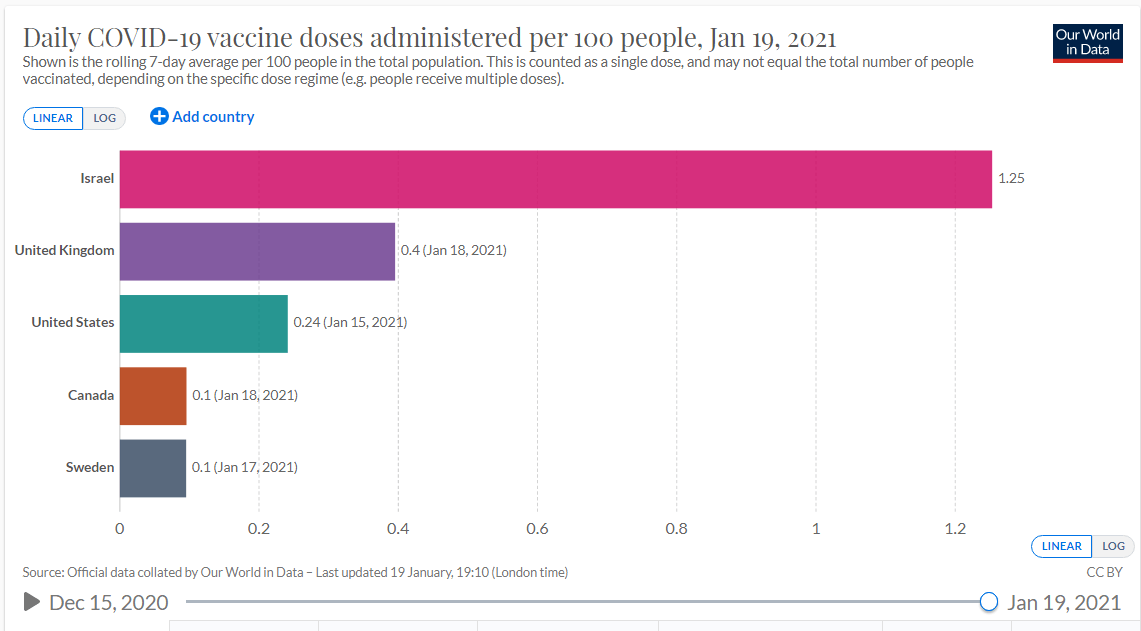

The pandemic’s second wave has hit Canada very hard, and the vaccine rollout has been disappointing (see chart below). Today’s MPR predicts that the economy will contract in the first quarter of this year. Economic weakness could be exacerbated by the Canadian dollar’s strength, which moved to above 79 cents US following today’s BoC announcement. Ten-year yields edged up modestly as well.

Bottom Line

For the year as a whole, economic growth is expected to be around 4% in 2021, compared to a contraction of -5.5% last year. As the inoculated population grows, the Bank forecasts an acceleration in growth to just under 5% in 2022 and a more-normal 2.5% in 2023. According to the January MPR, “The medium-term outlook is stronger than in the October Report because of vaccines’ positive effects, greater fiscal stimulus, stronger foreign demand and higher commodity prices. Meanwhile, potential output has also been revised up, reflecting an improved projection for business investment and less scarring effects on businesses and workers. There is considerable uncertainty around the medium-term outlook for GDP and the path for potential output. Thus, while the output gap is expected to close in 2023, the timing is particularly uncertain.”

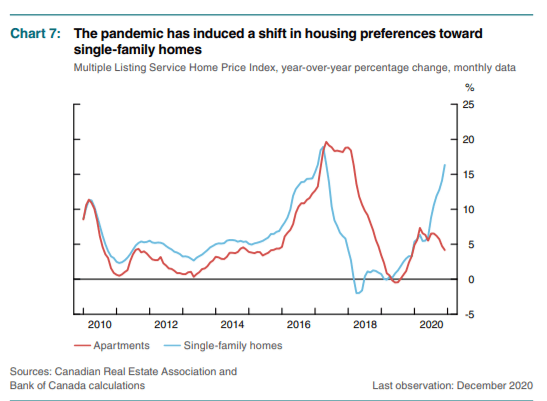

Concerning housing activity, the report said, “Demand for housing has continued to show resilience, despite increasing case numbers and tightening restrictions. Housing activity should remain elevated into the start of 2021, supported by low borrowing rates and resilient disposable incomes. Changes in homebuyers’ preferences have also played a role. For example, price growth has been strongest for single-family homes and in areas outside city centers,” shown in the chart below.

This article was written by DLC's Chief Economist Dr Sherry Cooper and was syndicated with permission.